The process of reconciling a bank statement worksheet can often feel like a daunting task, especially for individuals or businesses unfamiliar with financial accounting. It’s a crucial step in ensuring accuracy and identifying discrepancies between your bank account and your records. This guide will break down the process, offering practical tips and strategies to streamline the reconciliation process and minimize errors. Reconciling a bank statement worksheet is more than just a simple comparison; it’s a methodical approach to uncovering potential issues and maintaining financial integrity. Understanding the nuances of this process is essential for anyone managing their finances effectively. A well-executed reconciliation can prevent costly errors, protect your business from fraud, and provide a clear picture of your financial position. Let’s explore the key steps involved and the tools you’ll need to succeed.

Understanding the Basics of Bank Statements

Before diving into the reconciliation process, it’s important to grasp the fundamental concepts involved. A bank statement worksheet is a detailed record of all transactions that have occurred at your bank account. These statements typically include a wide range of transactions, such as deposits, withdrawals, transfers, and payments. The worksheet is organized into various sections, each representing a specific type of transaction. Understanding the different sections and their associated codes is critical for accurate reconciliation. Different banks use slightly different terminology and formatting, so it’s vital to familiarize yourself with the specific format used by your bank. Furthermore, the worksheet often includes a detailed description of each transaction, providing valuable context for identifying discrepancies. The goal of reconciliation is to match the information on the bank statement with your own records, ensuring that all transactions are accounted for and that there are no missing or incorrect entries.

Step 1: Gathering Your Records

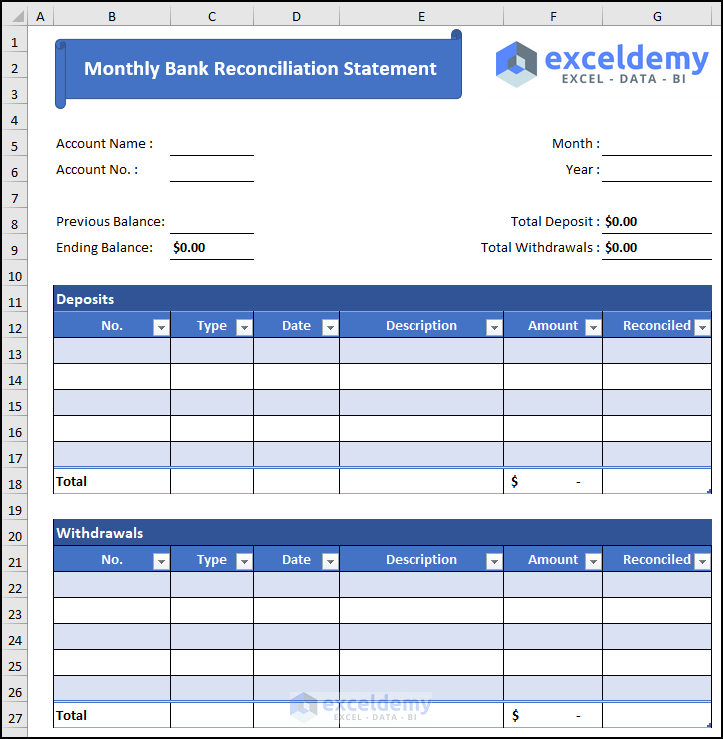

The first step in the reconciliation process is to gather all your records. This includes your bank statements, your accounting records, and any other relevant documents. It’s crucial to maintain a clear and organized system for storing these records. Consider using a spreadsheet or accounting software to track your transactions and ensure that you have all the necessary information readily available. Make sure to keep copies of your bank statements and your accounting records, as you may need to refer to them during the reconciliation process. Double-check that all your records are accurate and complete before proceeding with the reconciliation. A thorough review of your records will help you identify any potential discrepancies and ensure that you’re reconciling the correct information. Don’t underestimate the importance of meticulous record-keeping – it’s the foundation of a successful reconciliation.

Step 2: Initial Review – Spotting Immediate Issues

The initial review of the bank statement worksheet is often the most time-consuming part of the process. It’s important to look for obvious errors, such as missing transactions or incorrect amounts. Pay close attention to transactions that appear unusual or that don’t seem to match your records. For example, if you notice a large withdrawal that doesn’t appear on your bank statement, it’s a potential red flag. Also, carefully examine transactions that are significantly different from your usual patterns. These discrepancies may indicate errors in your records or fraudulent activity. Don’t dismiss anything at first glance; a quick review can often uncover significant issues. Document all your initial observations and discrepancies, as this information will be invaluable during the reconciliation process.

Step 3: Detailed Comparison – Matching Transactions

Once you’ve identified some initial issues, it’s time to perform a detailed comparison of the bank statement worksheet with your accounting records. This involves matching each transaction on the bank statement with its corresponding entry in your accounting system. This is where the Reconciling a bank statement worksheet really comes into play. Carefully compare the amounts, dates, and descriptions of each transaction. Look for any discrepancies, such as incorrect amounts, missing transactions, or duplicate entries. Use a spreadsheet to track your findings and ensure that you’re not overlooking any discrepancies. It’s helpful to create a table that lists each transaction, the bank statement amount, and your accounting record amount. This will make it easier to identify and resolve any discrepancies. Remember to consider the date of the transaction and ensure that it matches the date recorded on your accounting records.

Step 4: Investigating and Resolving Discrepancies

Once you’ve identified discrepancies, it’s time to investigate and resolve them. The root cause of the discrepancy may be simple, such as a typo in your records, or it may be more complex, such as a fraudulent transaction. Depending on the nature of the discrepancy, you may need to contact your bank to clarify the transaction. If the discrepancy is due to an error in your records, you’ll need to correct the error and update your accounting records. If the discrepancy is due to fraud, you’ll need to report it to the appropriate authorities. Document all your investigations and resolutions, as this information will be important for future reconciliation efforts. Don’t hesitate to seek professional advice if you’re unsure how to handle a complex discrepancy.

Step 5: Adjusting Balances – Correcting Errors

After resolving any discrepancies, you’ll need to adjust the balances in your accounting records to match the bank statement worksheet. This involves transferring the difference between the bank statement amount and your accounting record amount. Be careful to ensure that you’re only adjusting the correct balances and that you’re not making any other adjustments. Always document your adjustments, as this will provide a clear record of how the reconciliation was performed. Double-check your adjustments to ensure that they are accurate and that you’re not making any errors. A meticulous approach to adjusting balances is essential for maintaining the accuracy of your financial records.

Step 6: Review and Confirmation – Final Check

Before finalizing the reconciliation, it’s important to review the entire process to ensure that it was conducted accurately and completely. This includes checking your records, comparing the bank statement worksheet with your accounting records, and verifying that all discrepancies have been resolved. Ask a colleague to review your reconciliation to ensure that it’s accurate and that you haven’t missed any important details. A final confirmation is crucial to ensure that the reconciliation is complete and accurate. This step also provides an opportunity to identify any potential areas for improvement in your reconciliation process. A well-executed reconciliation is a testament to your attention to detail and your commitment to accurate financial reporting.

Conclusion

Reconciling a bank statement worksheet is a vital process for maintaining accurate financial records. It requires careful attention to detail, a systematic approach, and a commitment to accuracy. By following the steps outlined in this guide, you can streamline the reconciliation process, minimize errors, and ensure that your financial statements are reliable and trustworthy. Remember that a well-executed reconciliation is an investment in your financial health. The consistent application of these techniques will significantly reduce the risk of errors and improve your overall financial management. Ultimately, a robust reconciliation process empowers you to make informed decisions based on accurate financial data. Continuous improvement in your reconciliation methods is key to long-term financial stability. Don’t underestimate the power of a well-maintained reconciliation system.

Additional Resources

- Accounting Software Tutorials: [Insert Link to a helpful accounting software tutorial resource here]

- Bank Statement FAQs: [Insert Link to a reputable bank statement FAQ resource here]

- Financial Statement Best Practices: [Insert Link to a resource on best practices for financial statement preparation]