The process of reconciling a bank statement worksheet can often feel like a daunting task, especially for individuals or businesses unfamiliar with financial accounting. It’s a crucial step in ensuring accuracy and identifying discrepancies between your bank account and your records. This guide will break down the process, offering practical tips and strategies to streamline the reconciliation process and minimize errors. Reconciling a bank statement worksheet is a fundamental activity for maintaining financial stability and detecting potential fraud. Understanding the nuances of this process is essential for anyone managing their finances. A well-executed reconciliation can save you significant time, money, and potential headaches. Let’s explore the key steps involved.

Understanding the Basics

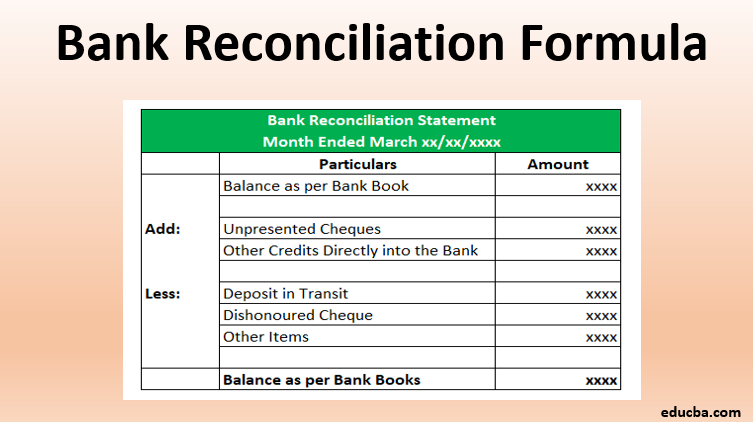

Before diving into the reconciliation process, it’s important to grasp the fundamental concepts involved. A bank statement worksheet is a detailed record of all transactions that have occurred at your bank account. It typically includes a chronological list of deposits, withdrawals, transfers, and other activities. The worksheet is often generated by your bank and provides a snapshot of your account activity. It’s crucial to understand that the worksheet is a snapshot in time, and discrepancies can arise due to errors, omissions, or simply variations in how transactions are recorded. The goal of reconciliation is to identify and resolve these discrepancies, ensuring that your records accurately reflect your financial position. Different banks may use slightly different formats, so familiarize yourself with your bank’s specific worksheet requirements.

Step 1: Gathering Your Records

The first step in the reconciliation process is to gather all your financial records. This includes:

- Your Bank Statement: This is the primary source of information.

- Your Accounting Software: Software like QuickBooks, Xero, or similar platforms often automatically generate bank statements and can be used for reconciliation.

- Your Transaction Records: This includes any other records that may relate to your transactions, such as receipts, invoices, and payment confirmations.

- Supporting Documentation: Keep copies of all supporting documentation, such as invoices, checks, and payment confirmations.

It’s vital to maintain a clear and organized system for storing these records. A well-structured filing system will make the reconciliation process much easier and more efficient.

Step 2: Initial Review – Spotting Potential Issues

Once you have gathered your records, it’s time to perform an initial review. This involves looking for obvious discrepancies. Common issues to watch out for include:

- Unexplained Deposits: A large or unusual deposit that doesn’t match your records.

- Unexplained Withdrawals: A large or unusual withdrawal that doesn’t seem to be related to a transaction.

- Incorrect Amounts: Transactions that are significantly different from your records.

- Missing Transactions: Transactions that are not reflected in your records.

Don’t immediately assume a problem; a thorough review is necessary to identify potential issues. It’s often helpful to start with the most significant discrepancies and then work your way through the worksheet.

Step 3: Detailed Reconciliation – Matching Transactions

This is the core of the reconciliation process. You’ll need to meticulously match your bank statement with your accounting records. This involves comparing each transaction to its corresponding entry in your accounting software or transaction records.

- Deposits: Verify that the amount of the deposit matches the amount recorded in your accounting system.

- Withdrawals: Confirm that the amount of the withdrawal matches the amount recorded in your accounting system.

- Transfers: Ensure that the transfer from one account to another is correctly reflected in both systems.

- Recurring Transactions: Carefully review recurring transactions (e.g., monthly payments) to ensure they are accurately reflected.

Pay close attention to the date and time of each transaction. Even small discrepancies can be significant. Use the bank’s reconciliation worksheet as a guide, but always verify each transaction individually.

Step 4: Investigating and Resolving Discrepancies

After you’ve completed the initial review, you’ll likely uncover some discrepancies. It’s important to investigate these issues thoroughly.

- Contact Your Bank: Contact your bank to inquire about any discrepancies. They may be able to provide additional information or clarification.

- Review Transaction Details: Carefully examine the details of each transaction to determine the cause of the discrepancy.

- Check for Errors: Look for potential errors in your own records. Double-check your entries and ensure that all information is accurate.

- Trace Transactions: If a transaction is unclear, trace it back to its source to determine where it originated.

Step 5: Documentation and Reporting

Once you’ve resolved all discrepancies, it’s crucial to document the process and report the findings. This includes:

- Reconciliation Report: Create a detailed reconciliation report that summarizes the discrepancies identified and the steps taken to resolve them.

- Record of Discrepancies: Maintain a record of all discrepancies, including the date, description, and resolution.

- Communication: Communicate the findings to relevant parties, such as your bank and your accountant.

The Importance of Automation

Modern banking systems often offer automated reconciliation tools. These tools can significantly speed up the reconciliation process and reduce the risk of errors. However, it’s still important to perform a manual review of the results to ensure accuracy.

Conclusion

Reconciling a bank statement worksheet is a systematic process that requires attention to detail and a thorough understanding of financial accounting principles. By following these steps, you can effectively identify and resolve discrepancies, ensuring the accuracy of your financial records and maintaining a strong financial foundation. Remember that a proactive approach to reconciliation is key to preventing costly errors and maintaining financial stability. Properly managing your bank statement worksheet is an investment in the long-term health of your business or personal finances. Don’t underestimate the value of a well-executed reconciliation process.

Conclusion

The reconciliation of a bank statement worksheet is a critical process for maintaining accurate financial records. It involves gathering, reviewing, and meticulously matching transactions between your bank account and your accounting system. By following a structured approach, you can identify and resolve discrepancies, ensuring the accuracy of your financial statements and safeguarding your financial well-being. Continuous monitoring and proactive attention to this process are essential for maintaining a stable and reliable financial position. Ultimately, a robust reconciliation process empowers you to make informed financial decisions and navigate the complexities of managing your money effectively.