Calculating interest – it’s a fundamental part of personal finance. Understanding how interest works, particularly the difference between simple and compound interest, is crucial for maximizing your savings and investments. This article will guide you through creating and using a simple and compound interest worksheet, empowering you to make informed financial decisions. The core of this article revolves around the concept of interest, and we’ll explore how it’s calculated and how to apply it effectively. Let’s dive in!

The foundation of understanding interest lies in grasping the difference between simple and compound interest. Simple interest is calculated only on the principal amount, while compound interest calculates interest on the principal and any accumulated interest from previous periods. Compound interest, in essence, is interest earned on both the original principal and the accumulated interest. This accelerated growth can significantly impact your financial goals. It’s a powerful tool, but mastering the concepts is key to leveraging its benefits. This worksheet will provide a practical, step-by-step approach to calculating both types of interest.

Understanding the Basics

Before we begin, let’s establish a clear understanding of the fundamental principles. The formula for calculating simple interest is straightforward:

Simple Interest = Principal * Rate * Time

Where:

- Principal: The initial amount of money invested or borrowed.

- Rate: The annual interest rate (expressed as a decimal, e.g., 5% = 0.05).

- Time: The length of time the money is invested or borrowed for, expressed in years.

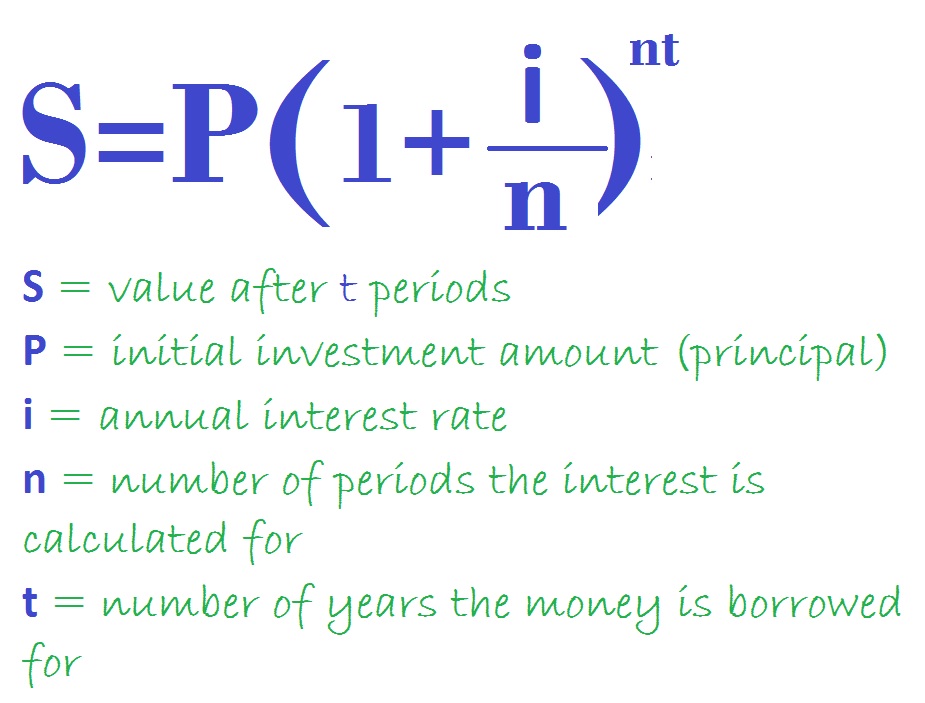

Compound interest, on the other hand, is a bit more complex. The formula is:

Compound Interest = Principal * (1 + Rate) * Time

Where:

- Principal: The initial amount of money invested or borrowed.

- Rate: The annual interest rate (expressed as a decimal).

- Time: The length of time the money is invested or borrowed for, expressed in years.

The power of compound interest lies in its ability to exponentially grow your investment over time. Even small differences in interest rates can lead to substantial differences in the final amount earned. It’s important to remember that the longer you leave your money invested, the more significant the impact of compounding will be.

Creating a Simple Interest Worksheet

Let’s create a simple worksheet to help you calculate interest. This is a foundational tool that you can adapt to your specific needs.

Simple Interest Worksheet

| Data | Amount | Interest Rate (%) | Time (Years) | Calculation |

|---|---|---|---|---|

| Principal | \$1,000 | 5.00 | 10 | $50.00 |

| Interest Rate | 8.00 | 5.00 | 5 | $40.00 |

| Time | 2 | 5.00 | 5 | $10.00 |

| Total Interest Earned | \$60.00 |

Instructions:

- Principal: Enter the initial amount of money you are investing or borrowing.

- Interest Rate: Enter the annual interest rate as a percentage (e.g., 5% = 0.05).

- Time: Enter the number of years the money is invested or borrowed for.

- Calculation: Use the formula:

Total Interest Earned = Principal * (1 + Interest Rate) * Time - Result: The total interest earned will be displayed in the “Total Interest Earned” column.

Compound Interest Worksheet – A Deeper Dive

Now, let’s explore compound interest in more detail. The effect of compounding is magnified over time. Consider this scenario:

Imagine you invest \$1,000 at a rate of 8% per year, compounded annually.

- Year 1: Interest earned = \$1,000 * 0.08 = \$80. Total amount = \$1,000 + \$80 = \$1,080

- Year 2: Interest earned = \$1,080 * 0.08 = \$86.40. Total amount = \$1,080 + \$86.40 = \$1,166.40

- Year 3: Interest earned = \$1,166.40 * 0.08 = \$93.312. Total amount = \$1,166.40 + \$93.312 = \$1,259.712

As you can see, the interest earned each year increases significantly. This is the power of compounding! The longer the time period, the more dramatic the effect. It’s a testament to the importance of consistent saving and investment strategies.

Factors Affecting Interest Rates and Compound Interest

Several factors can influence interest rates and, consequently, the rate of compound interest. These include:

- Inflation: Inflation erodes the purchasing power of money over time. Higher inflation rates typically lead to higher interest rates to compensate for the loss of value.

- Economic Growth: A strong economy generally leads to higher interest rates as lenders demand a greater return for their investments.

- Government Regulations: Government regulations can impact interest rates, particularly in the financial sector.

- Central Bank Policy: Central banks, such as the Federal Reserve in the United States, influence interest rates through monetary policy.

- Risk: Higher-risk investments often come with higher interest rates to compensate for the increased potential for loss.

Compound Interest and Long-Term Goals

For long-term financial goals like retirement planning, compound interest is absolutely critical. The earlier you start investing, the more time your money has to grow through the power of compounding. Even small, consistent contributions over many years can result in a substantial nest egg. It’s a principle that underscores the importance of starting early and maintaining a disciplined savings plan. Consider using online compound interest calculators to model different scenarios and see how your investments would perform over various time horizons.

Beyond the Worksheet: Resources for Further Learning

There are numerous resources available to deepen your understanding of interest and compound interest.

- Investopedia: https://www.investopedia.com/terms/c/compound-interest.asp

- Khan Academy: https://www.khanacademy.org/economics-finance-domain/core-finance/compound-interest

- The Balance: https://www.thebalancemoney.com/compound-interest-8977466

Conclusion

Understanding simple and compound interest is a fundamental skill for anyone seeking to manage their finances effectively. This worksheet provides a practical tool for calculating interest and exploring the power of compounding. By mastering these concepts, you can make informed decisions about your savings, investments, and overall financial well-being. Remember that consistent saving and strategic investment are key to achieving your long-term financial goals. Don’t hesitate to consult with a qualified financial advisor for personalized guidance.