Balancing a checkbook is a fundamental skill for managing personal finances effectively. It’s more than just keeping track of income and expenses; it’s about understanding how your money flows, identifying areas for savings, and ensuring you’re not overdrawing your accounts. A well-executed checkbook worksheet can significantly reduce financial stress and provide a clear roadmap for your financial goals. This guide will walk you through creating and utilizing a checkbook worksheet, empowering you to take control of your money. Balancing A Checkbook Worksheet is a powerful tool for anyone looking to gain a deeper understanding of their financial situation and make informed decisions. It’s a simple yet incredibly effective method for maintaining financial stability and achieving long-term financial security. Let’s dive in.

Understanding the Basics

Before we begin constructing a checkbook worksheet, it’s essential to grasp the core principles. A checkbook worksheet is a detailed record of all your income and expenses, categorized and tracked. It’s not a rigid set of rules, but rather a flexible framework to help you visualize your spending habits and identify potential areas for improvement. The goal is to maintain a balance between your income and expenses, ensuring you have enough money to cover your obligations and save for the future. It’s a proactive approach to managing your finances, rather than a reactive one. A good checkbook worksheet is a living document, constantly updated as your financial situation changes.

Setting Up Your Checkbook Worksheet

The first step in creating a checkbook worksheet is to gather your financial information. This typically includes:

- Income: List all sources of income – salary, wages, investments, side hustles, etc. Be as specific as possible.

- Expenses: Categorize your expenses into fixed (rent/mortgage, utilities, insurance) and variable (groceries, entertainment, dining out) categories. Track your spending diligently for at least a month to get a clear picture.

- Savings: Record all savings accounts and the amount you’ve saved.

There are numerous templates available online – you can find free ones readily accessible. However, it’s crucial to customize the worksheet to fit your individual needs and circumstances. Consider using a spreadsheet program like Excel or Google Sheets for ease of use and data management. A simple table format is often the most effective.

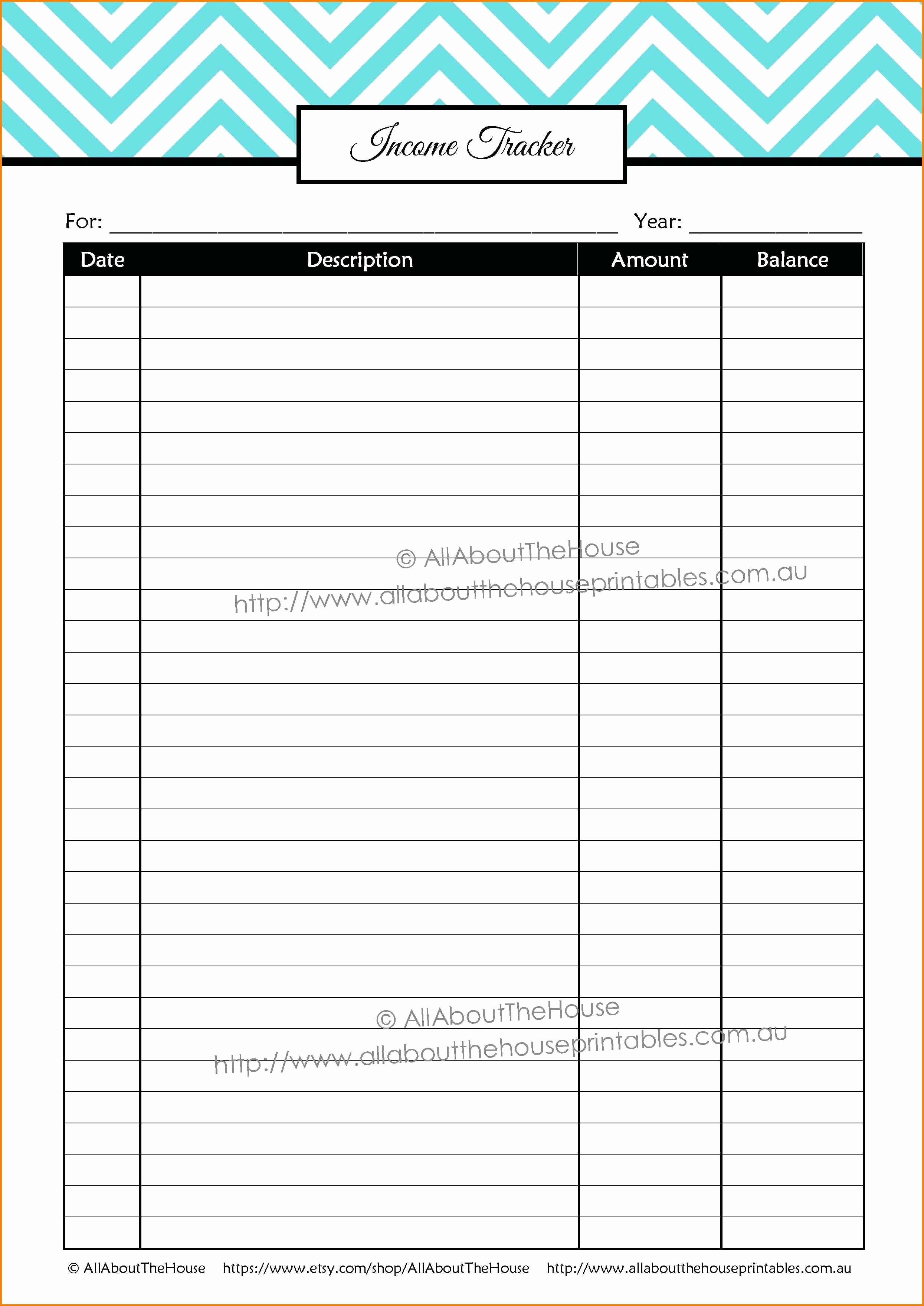

Income Tracking – The Foundation

Accurate income tracking is the cornerstone of any effective checkbook worksheet. It’s vital to know exactly how much money you’re bringing in each month. Don’t underestimate the power of a clear record of all income sources. Consider using a dedicated bank account or a separate savings account for income to keep your personal finances separate. Regularly reviewing your income data allows you to identify any discrepancies or unexpected sources of funds. Balancing A Checkbook Worksheet relies heavily on accurate income data; inaccurate figures will lead to inaccurate tracking and potentially flawed financial planning.

Expenses – Categorizing and Analyzing

Once you’ve tracked your income, it’s time to analyze your expenses. Categorizing your spending helps you identify areas where you can cut back. Common expense categories include:

- Housing: Rent/Mortgage, Property Taxes, Homeowners Insurance

- Utilities: Electricity, Gas, Water, Trash

- Transportation: Car Payments, Gas, Insurance, Public Transportation

- Food: Groceries, Dining Out

- Healthcare: Insurance Premiums, Doctor Visits, Medications

- Debt Payments: Credit Card Payments, Student Loans, Personal Loans

- Entertainment: Movies, Concerts, Hobbies

- Personal Care: Haircuts, Cosmetics, Gym Memberships

- Miscellaneous: Uncategorized expenses – these are important to track!

Analyzing your spending patterns is key to identifying areas where you can reduce unnecessary expenses. Tools like budgeting apps can automate this process, but a manual review is often necessary. Don’t just track; understand where your money is going.

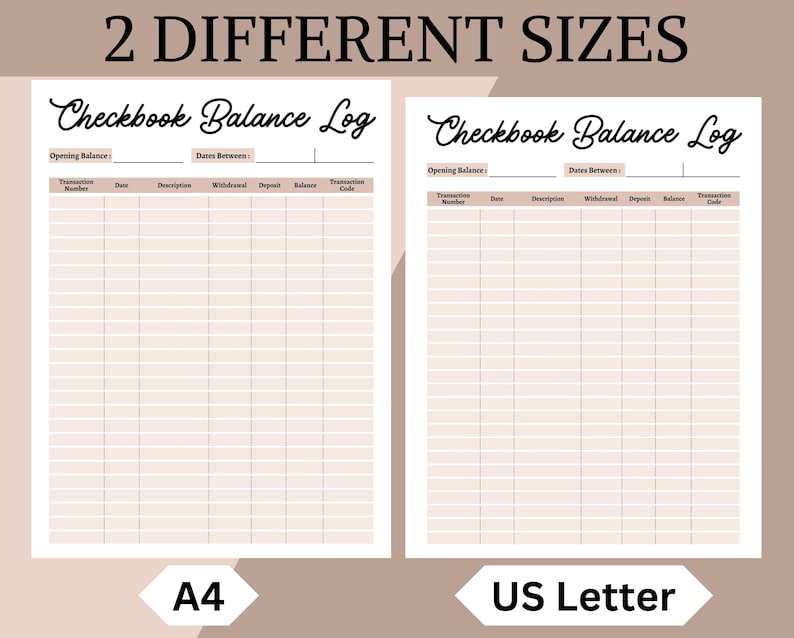

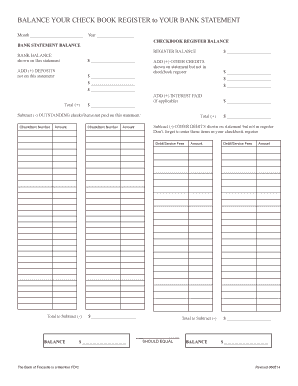

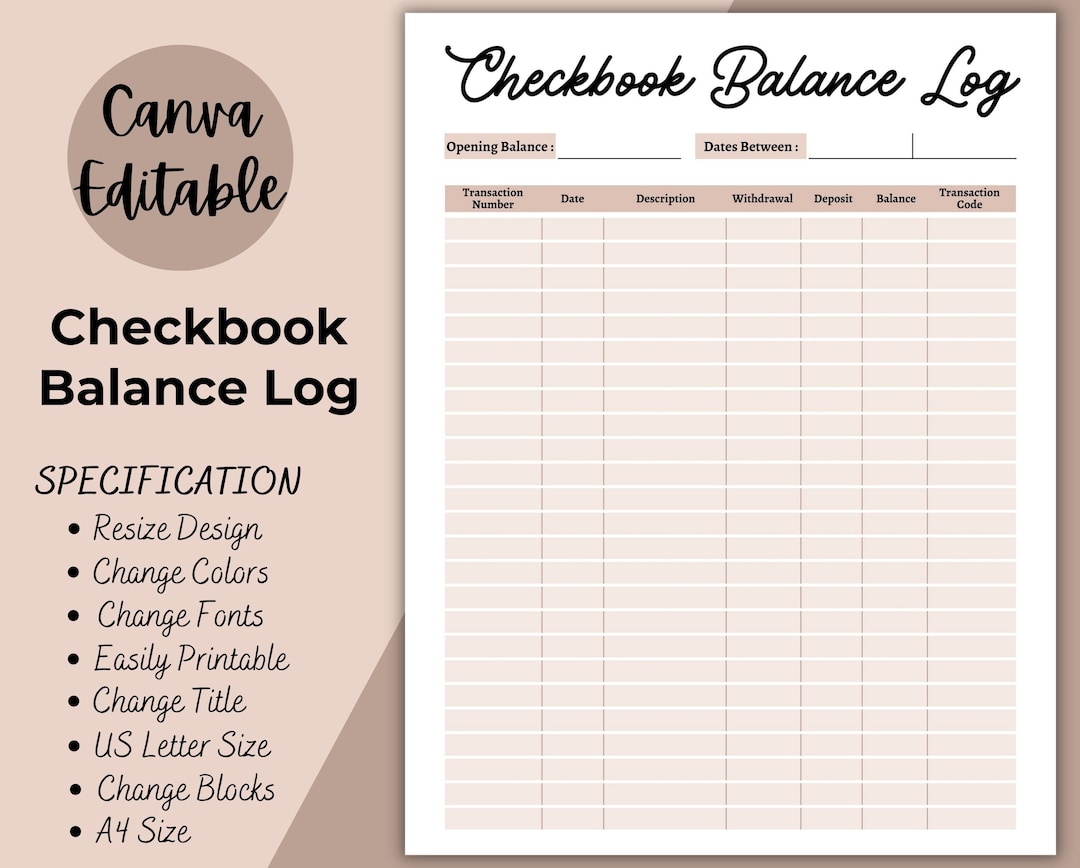

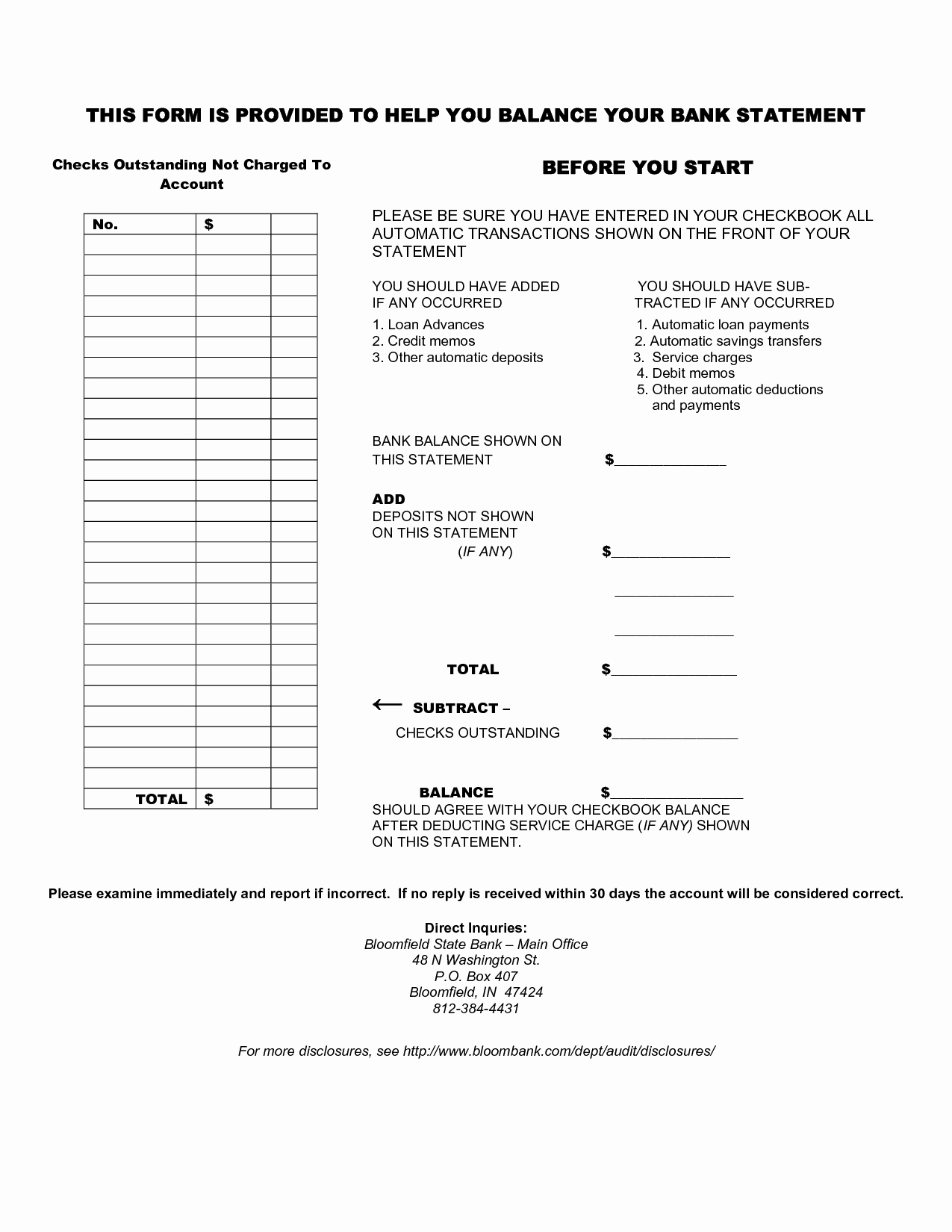

Balancing Your Accounts – The Core of the Worksheet

The heart of the checkbook worksheet lies in the balance. This is the difference between your income and your expenses. A positive balance means you have more income than expenses, indicating a surplus. A negative balance means you have more expenses than income, requiring adjustments. The goal is to maintain a consistent balance, ideally with a small surplus to allow for savings and investments. It’s important to regularly review your balance and make adjustments as needed.

The “Balance” Column – A Visual Guide

The “Balance” column is crucial for visualizing your financial health. It’s a simple table that shows your income, expenses, and the resulting balance. This visual representation makes it easy to identify potential problems and track your progress. A consistently positive balance is a sign of financial stability. A consistently negative balance signals that you need to re-evaluate your spending habits.

Tracking Surplus and Deficit

It’s not just about the balance; it’s about understanding why it exists. A surplus means you’re spending less than you earn. A deficit means you’re spending more than you earn. The worksheet should prompt you to investigate the root causes of these imbalances. Are you overspending in certain categories? Are you consistently missing a payment? Are you consistently saving?

Adjusting Your Budget – Making Changes

Based on your analysis, you’ll likely need to adjust your budget. This might involve cutting back on discretionary spending, increasing your savings rate, or negotiating lower rates on your bills. Balancing A Checkbook Worksheet encourages you to be proactive in making these adjustments. Small changes can add up to significant savings over time.

The Importance of Regular Review and Updates

A checkbook worksheet isn’t a one-time exercise; it’s a living document. It’s essential to review and update your worksheet regularly – at least monthly, and ideally more frequently. As your income, expenses, and financial goals change, your worksheet needs to adapt accordingly. This ensures that your financial plan remains relevant and effective. Don’t let your worksheet become a dusty relic of the past. Regular updates are key to maintaining a healthy financial relationship with your money.

Leveraging the Worksheet for Financial Goals

The checkbook worksheet is a powerful tool for achieving specific financial goals. For example, if you’re saving for a down payment on a house, you can use the worksheet to track your progress and make adjustments to your savings plan. If you’re trying to pay off debt, you can use the worksheet to identify areas where you can accelerate your debt repayment. Balancing A Checkbook Worksheet provides a structured framework for setting and achieving these goals.

Conclusion

Creating and utilizing a checkbook worksheet is a fundamental step towards achieving financial stability and achieving your financial goals. It’s a simple, yet incredibly effective method for understanding your money, identifying areas for improvement, and making informed decisions. By diligently tracking your income and expenses, analyzing your spending patterns, and regularly reviewing and updating your worksheet, you can gain a clear picture of your financial health and take control of your future. Remember, the key to success is consistency and a proactive approach to managing your finances. A well-maintained checkbook worksheet is an investment in your long-term financial well-being. Don’t underestimate the power of this simple tool.

Conclusion

Ultimately, the checkbook worksheet is more than just a financial record; it’s a tool for empowerment. It’s a mechanism for gaining control, understanding your finances, and making conscious choices that align with your goals. By consistently utilizing this method, individuals can significantly improve their financial health and build a more secure future. The process of creating and maintaining a checkbook worksheet is a continuous journey of self-awareness and financial responsibility. It’s a commitment to taking charge of your money and creating a life of financial freedom.